- March 02, 2026

Kotak Mahindra Bank vs HDFC Bank: Faster Loan Growth Meets Margin Pressure in Q3 FY26

Kotak Mahindra Bank outpaced HDFC Bank in loan growth in Q3 FY26, but margin pressure highlights the trade-off between growth and efficiency.

- January 25, 2026

- in Business

Kotak Mahindra Bank and HDFC Bank, two of India’s most closely tracked private lenders, delivered contrasting performances in the December 2025 quarter, underscoring a familiar banking dilemma in a softening interest rate cycle: growth versus margins.

With the Reserve Bank of India beginning a monetary easing phase in late 2025, investors were keenly watching how leading banks would balance credit expansion with profitability. The latest quarterly numbers reveal that while Kotak Mahindra Bank surged ahead in loan growth, it did so at the cost of some margin compression—an issue HDFC Bank also faced, albeit with a more conservative growth strategy.

Loan Growth: Kotak Takes the Lead

Kotak Mahindra Bank reported year-on-year loan growth of 16.2% in Q3 FY26, significantly higher than HDFC Bank’s 12% expansion during the same period. Kotak’s advances reached approximately ₹4.8 lakh crore, driven largely by strong traction in retail lending, including personal loans, consumer durable financing, and business banking assets.

Analysts note that these retail-heavy segments typically offer higher yields compared to large corporate loans, helping banks cushion margin pressure in a falling rate environment. Kotak’s focus on such high-yield segments allowed it to sustain one of the strongest growth profiles among private sector banks.

HDFC Bank, on the other hand, remained cautious in growing its loan book following its merger-related balance sheet adjustments. With a loan-to-deposit ratio still above 90%, the bank prioritised stability over aggressive expansion. Its retail loans grew 6.9%, while small and mid-market enterprise loans rose 17.2%, reflecting selective risk-taking.

Margins Under Pressure

Both banks saw a decline in net interest margins (NIMs), reflecting the impact of RBI’s rate cuts and competitive pricing. Kotak Mahindra Bank’s NIM slipped to 4.5% in Q3 FY26 from 4.9% a year earlier. Despite the decline, Kotak’s margins remain among the highest in the industry, comfortably ahead of most peers.

HDFC Bank’s NIM stood at 3.5%, slightly lower than the 3.6% recorded a year ago. The bank has acknowledged that margin normalisation is likely to continue in the near term as deposit costs remain elevated even as lending rates soften.

Asset Quality and Profitability

Asset quality remained a bright spot for both lenders. Kotak Mahindra Bank reduced its net non-performing assets (NPAs) to 0.31%, down from 0.4% a year earlier, supported by a provision coverage ratio of 76%. However, a one-time expense linked to the implementation of the new labour code weighed on profitability, limiting standalone net profit growth to 4% year-on-year.

HDFC Bank reported net NPAs of 0.42%, an improvement over the previous year. Lower provisions helped the bank post a stronger 11.5% growth in standalone net profit, reinforcing its reputation for steady earnings delivery even during periods of moderated growth.

Efficiency Metrics and Valuations

Both banks posted identical return on assets (RoA) of 0.48% for the quarter, translating to an annualised RoA of nearly 1.9%—among the best in the Indian banking sector. Valuations, however, tell a different story. Kotak Mahindra Bank continues to trade at a premium, reflecting investor confidence in its growth trajectory and asset quality. HDFC Bank trades at comparatively lower valuation multiples, appealing to investors seeking stability and predictable earnings.

Outlook

With the RBI planning additional liquidity injections and a supportive policy stance, credit growth across the banking sector is expected to remain healthy in the coming quarters. Investors will closely track how banks manage the delicate balance between expanding loan books and protecting margins in a lower-rate environment.

Kotak Mahindra Bank’s performance highlights the rewards—and risks—of faster growth, while HDFC Bank’s strategy underscores the value of caution and balance sheet strength. As the rate cycle evolves, the race between efficiency and expansion is set to define investor sentiment across banking stocks.

you may also like

- March 02, 2026

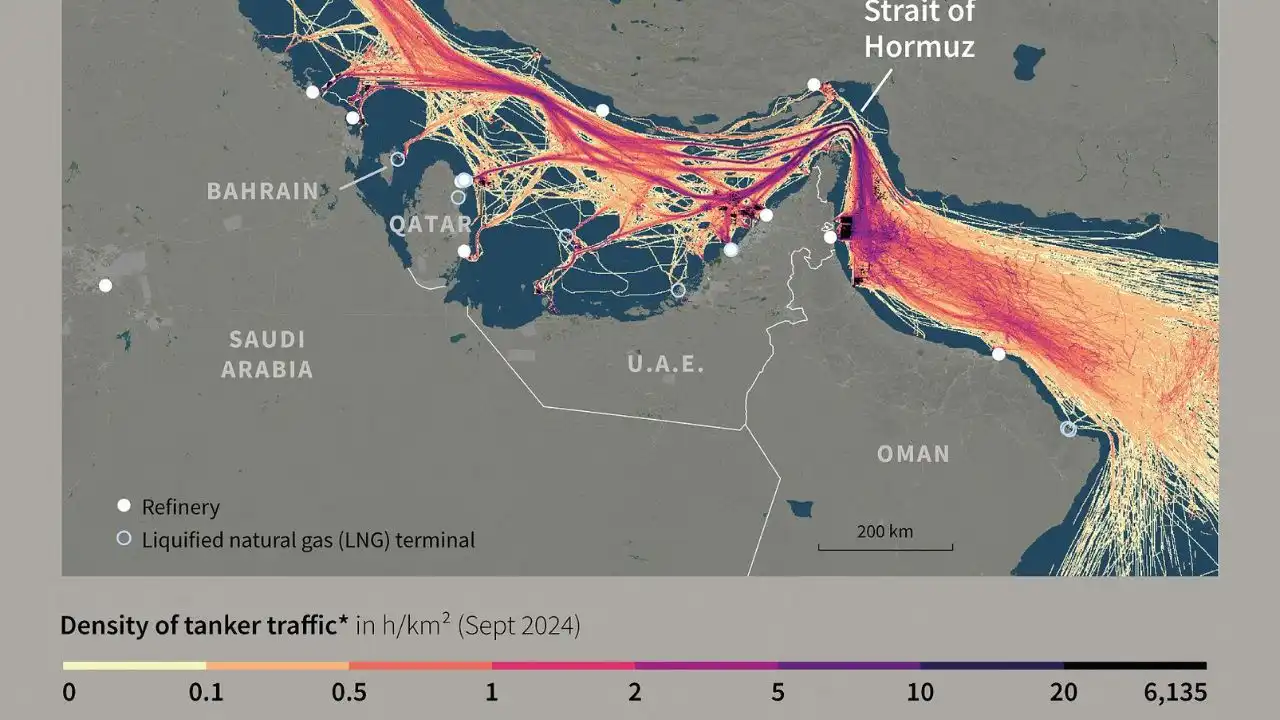

Middle East Tensions: Impact on India Trade & Oil

- March 02, 2026

Intel CEO Warns of Huawei’s Chip Talent Push

- February 28, 2026

Amazon to Invest $50B in OpenAI, Expands AWS Tie-Up

- February 28, 2026