- March 02, 2026

Q3 Earnings, US Fed Rate Call and Union Budget Set to Drive Market Sentiment This Week

Markets brace for a volatile week as Q3 results, the US Fed rate decision and the Union Budget shape investor sentiment.

- January 25, 2026

- in Business

Indian equity markets are heading into a highly eventful week, with multiple domestic and global triggers expected to dictate investor sentiment. Key factors likely to influence market movement include the ongoing third-quarter earnings season, the upcoming interest rate decision by the US Federal Reserve, and the presentation of the Union Budget for the financial year 2026–27.

Trading will resume after a holiday-shortened start to the week, as equity markets remain closed on Monday due to Republic Day. Attention is expected to intensify from Tuesday onward, with investors closely tracking macroeconomic indicators, foreign investor activity, and global developments.

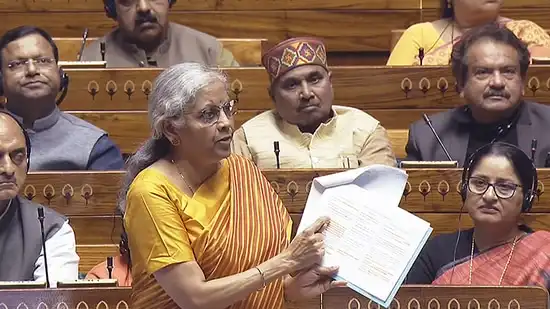

The Union Budget will be presented on February 1 by Finance Minister Nirmala Sitharaman. In a rare move, both National Stock Exchange and Bombay Stock Exchange will remain open for live trading on Sunday to allow markets to react in real time to the Budget announcements.

Analysts note that domestic factors such as industrial production data, fiscal indicators, and weekly foreign exchange reserves will be closely monitored. At the same time, corporate earnings will take centre stage, with results expected from several heavyweight companies across banking, infrastructure, automobiles, FMCG, and power sectors.

Globally, market focus remains firmly on the policy outlook of the US Federal Reserve, whose interest rate decision is due later this week. Investors are also watching US macroeconomic data releases, commentary from global central banks, and developments related to international trade policies, all of which could influence capital flows into emerging markets like India. Foreign portfolio investor (FPI) activity is expected to remain a critical variable. Recent sessions have seen sustained selling pressure from overseas investors, driven by a combination of factors including a weakening rupee, uncertainty around global trade negotiations, and muted earnings growth so far in the current quarter. The rupee recently slipped to a historic low against the US dollar, adding to concerns around currency stability and imported inflation.

Market participants are also keeping a close watch on global equity trends and crude oil prices, which continue to act as important sentiment drivers. Geopolitical tensions in parts of the Middle East and Europe have added to volatility in global risk assets, further influencing investor positioning.

With the Union Budget approaching, the market narrative is expected to shift decisively toward fiscal policy expectations. Investors are looking for growth-oriented measures aimed at reviving both domestic demand and foreign investor confidence. Key expectations include continued fiscal consolidation, a sustained push toward capital expenditure—particularly in infrastructure, defence, and railways—and targeted support for MSMEs and export-driven sectors facing global headwinds.

There is also anticipation around possible tax rationalisation, sector-specific incentives, and policy reforms designed to deepen capital markets and improve efficiency. Analysts suggest that if the Budget avoids major tax surprises, its immediate impact on equity markets may remain limited, with broader direction determined by earnings trends and global cues. Technically, some market experts believe a mild rebound cannot be ruled out as markets enter the pre-Budget and monthly derivatives expiry phase. Elevated short positions by foreign investors and oversold momentum indicators could lead to intermittent bouts of short covering, offering temporary relief to benchmark indices.

Last week, Indian markets ended sharply lower, weighed down by persistent foreign outflows, a depreciating currency, weak global cues, and underwhelming corporate earnings. Despite the near-term pressure, investors remain cautiously optimistic that policy clarity from the Budget and stabilisation in global conditions could help restore confidence in the weeks ahead.

As markets navigate this convergence of earnings, monetary policy, and fiscal announcements, volatility is expected to remain elevated, making the coming sessions critical for setting the near-term direction of Indian equities.

you may also like

- March 02, 2026

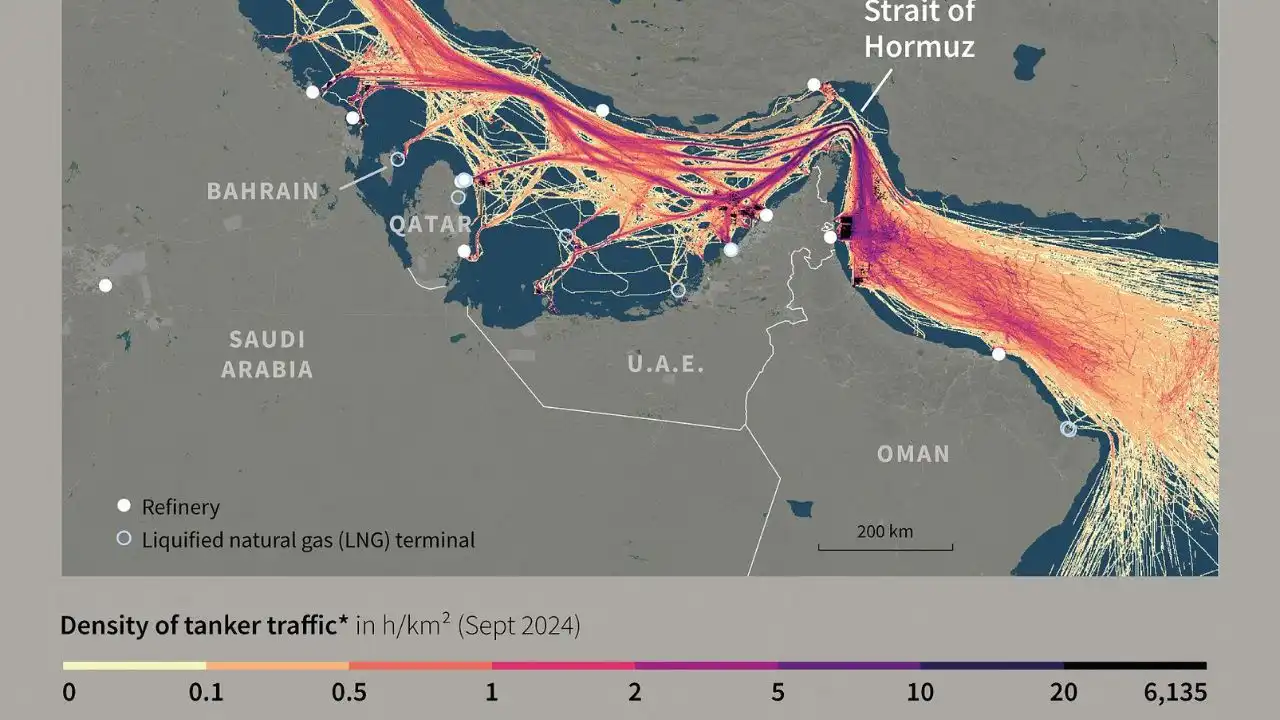

Middle East Tensions: Impact on India Trade & Oil

- March 02, 2026

Intel CEO Warns of Huawei’s Chip Talent Push

- February 28, 2026

Amazon to Invest $50B in OpenAI, Expands AWS Tie-Up

- February 28, 2026