- March 02, 2026

Swiggy Q3FY26: Revenue Jumps 54% as Losses Widen to ₹1,065 Crore, User Base Hits New High

Swiggy posts 54% revenue growth in Q3FY26 but net loss widens to ₹1,065 crore as user base and order value surge.

- January 29, 2026

- in Business

Food delivery and quick-commerce major Swiggy reported a sharp rise in revenue but deeper losses in the third quarter of FY26, highlighting the ongoing trade-off between rapid scale-up and profitability in India’s competitive consumer internet space.

For Q3FY26, Swiggy posted a consolidated net loss of ₹1,065 crore, widening from a loss of ₹799 crore in the same quarter last year. However, on a quarter-on-quarter basis, losses narrowed slightly from ₹1,092 crore in Q2FY26, signalling early signs of cost stabilisation.

Revenue growth remains the headline

Despite the widening loss, Swiggy’s top-line performance remained strong. Revenue from operations surged 53.9% year-on-year to ₹6,149 crore, compared to ₹3,993 crore in Q3FY25. Sequentially, revenue rose 10.6%, underlining sustained demand across its platforms.

This growth reflects Swiggy’s continued push across food delivery, quick commerce, and adjacent consumer services, even as competition intensifies and customer acquisition costs remain elevated.

User base expands sharply

A key positive in the quarter was Swiggy’s expanding customer base. The company reported:

-

Average monthly transacting users (MTU): 24.3 million, up 36.8% YoY

-

Sequential MTU growth of 5.9%, indicating consistent user engagement

The expansion suggests that Swiggy continues to penetrate deeper into both metro and non-metro markets, aided by faster delivery promises, discounts, and platform stickiness.

Food delivery still the core engine

Swiggy’s food delivery segment remained the backbone of its business. During the quarter:

-

Gross Order Value (GOV) grew 20.5% YoY to ₹8,959 crore

-

Food delivery MTUs increased 22% YoY to 18.1 million

While growth in food delivery is slower than newer verticals, it remains Swiggy’s most stable and predictable revenue driver, offering scale and recurring demand.

Margins: pressure remains, but sequential relief

On the profitability front, Swiggy’s B2C adjusted EBITDA margin came in at -3.5%:

-

Down 16 basis points YoY, reflecting higher operating and expansion costs

-

Improved 15 basis points sequentially, hinting at tighter cost controls

The marginal improvement quarter-on-quarter suggests that Swiggy is attempting to balance growth with efficiency, even as it continues to invest heavily in logistics, technology, and customer acquisition.

Why losses are still rising

The widening annual loss reflects multiple structural pressures:

-

Aggressive spending to defend market share

-

Rising delivery and rider costs

-

Continued investments in new business lines

-

Competitive discounting in food and quick commerce

While revenue growth remains strong, the path to profitability continues to depend on operating leverage, better unit economics, and moderation in incentive-led growth.

Bigger picture: scale vs sustainability

Swiggy’s Q3FY26 performance underscores a familiar theme in India’s digital consumer economy — growth is visible, scale is accelerating, but profitability remains elusive.

With over 24 million active users, rising order volumes, and strong revenue momentum, Swiggy has clearly cemented itself as a dominant platform. The challenge now lies in converting this scale into sustainable profits without losing momentum in an increasingly crowded market.

you may also like

- March 02, 2026

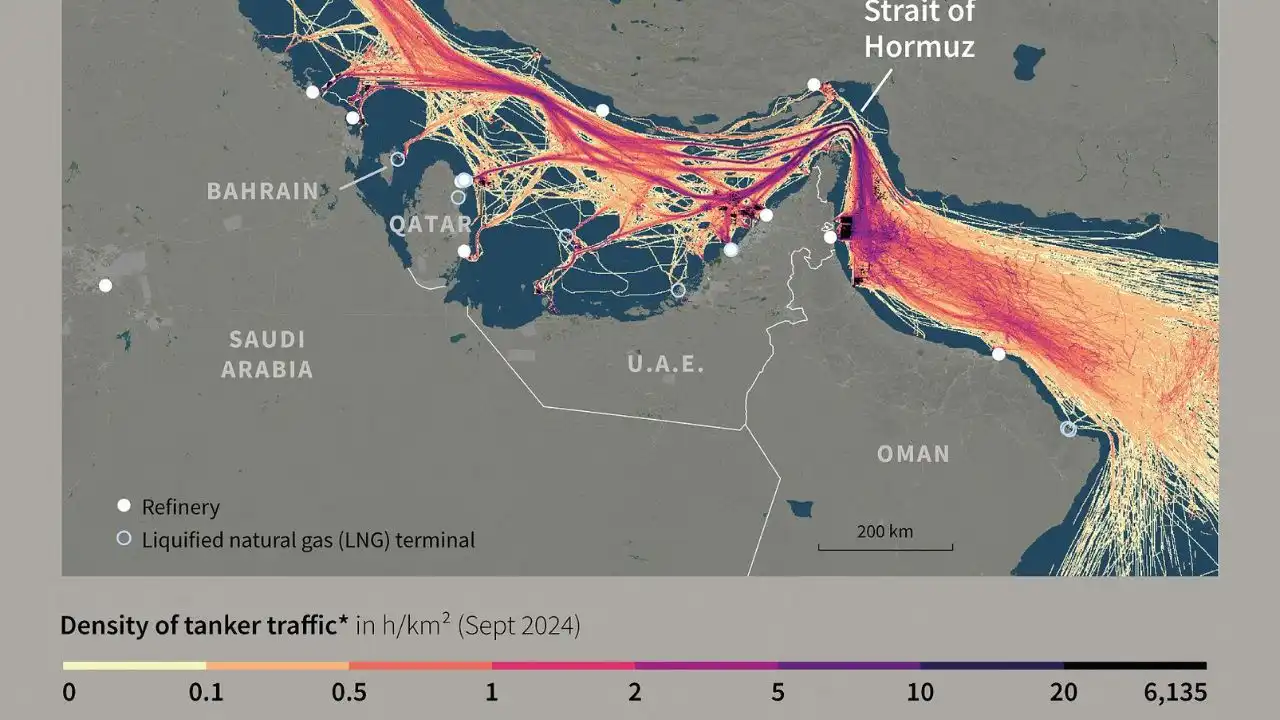

Middle East Tensions: Impact on India Trade & Oil

- March 02, 2026

Intel CEO Warns of Huawei’s Chip Talent Push

- February 28, 2026

Amazon to Invest $50B in OpenAI, Expands AWS Tie-Up

- February 28, 2026