- March 02, 2026

Why Over-Regulation Is Holding Back India’s Economic Breakthrough

India’s over-regulated economy limits manufacturing, exports, tourism and jobs. A deep dive into why reform, not protection, matters.

- February 10, 2026

- in Business

The temporary relief brought by the latest India-US trade understanding should not be mistaken for a structural victory. If anything, the turbulence caused by a year of tariff pressure has exposed a long-ignored truth: India remains one of the world’s most over-regulated and under-competitive major economies. The discomfort forced a moment of clarity that domestic debate has repeatedly postponed.

At the heart of the issue is not geopolitics or bad luck, but a system that protects inefficiency, rewards compliance over competence, and confuses control with capability.

Why India Never Had an Industrial Revolution Moment

Unlike East Asian economies that used manufacturing as a ladder out of poverty, India never completed a full industrial transition. Nearly 45 percent of India’s workforce remains stuck in agriculture, even though agriculture contributes a fraction of national income. Alarmingly, roughly half of these workers are effectively redundant — producing little additional output but trapped due to lack of alternatives.

Instead of absorbing surplus labour into factories, logistics, and export-oriented industries, India built a maze of licences, permissions, inspections, and compliance rituals that quietly discouraged scale. Small firms stayed small not by choice, but by design — because growing meant inviting regulatory attention.

The Export Failure No One Likes to Admit

India’s share of global goods exports sits at a modest 2 percent, an uncomfortable statistic for an economy that aspires to global leadership. This is not for lack of talent or entrepreneurship, but because exporting from India often means battling infrastructure gaps, complex taxation layers, unpredictable customs procedures, and regulatory uncertainty.

When global firms look for alternatives to China, logic suggests India should be the natural choice. Yet many choose Vietnam, a country with a far smaller domestic market. The reason is simple: Vietnam offers speed, clarity, and predictability — three things Indian regulation still struggles to deliver.

Protectionism as Policy Habit

For decades, India has relied on protectionism as a substitute for competitiveness. High tariffs, import restrictions, and regulatory barriers were meant to nurture domestic champions. Instead, they often produced sheltered firms unprepared for global competition.

The recent tariff shocks were uncomfortable precisely because they removed this cushion. Suddenly, inefficiency became expensive. The pressure exposed how deeply Indian policy still mistrusts markets, scale, and competition.

Tourism: A Global Missed Opportunity

Despite extraordinary natural landscapes, historical depth, and cultural diversity, India attracts just about 1.3 percent of global tourists. This is not a branding problem; it is a governance problem.

Tourists do not merely seek monuments — they seek clean infrastructure, predictable rules, safe mobility, and frictionless services. Over-regulation here translates into under-delivery: from airport bottlenecks to hotel licensing headaches to inconsistent local enforcement.

What the Economy Actually Wants

India does not need louder slogans or grander visions. It needs something far more mundane and far more radical:

-

Fewer rules, but clearer ones

-

Faster approvals instead of layered permissions

-

Trust in enterprise rather than suspicion of scale

-

Competition instead of comfort

-

Governance that enables, not supervises

The real lesson from tariff pain is not about trade partners. It is about internal reform fatigue. Growth does not emerge from insulation; it emerges from exposure.

The Bottom Line

India’s challenge is not lack of potential — it is regulatory excess choking momentum. Until the system shifts from control to confidence, the economy will continue to punch below its weight. Relief from global pressure may feel good, but forgetting the lesson would be the costliest mistake of all.

you may also like

- March 02, 2026

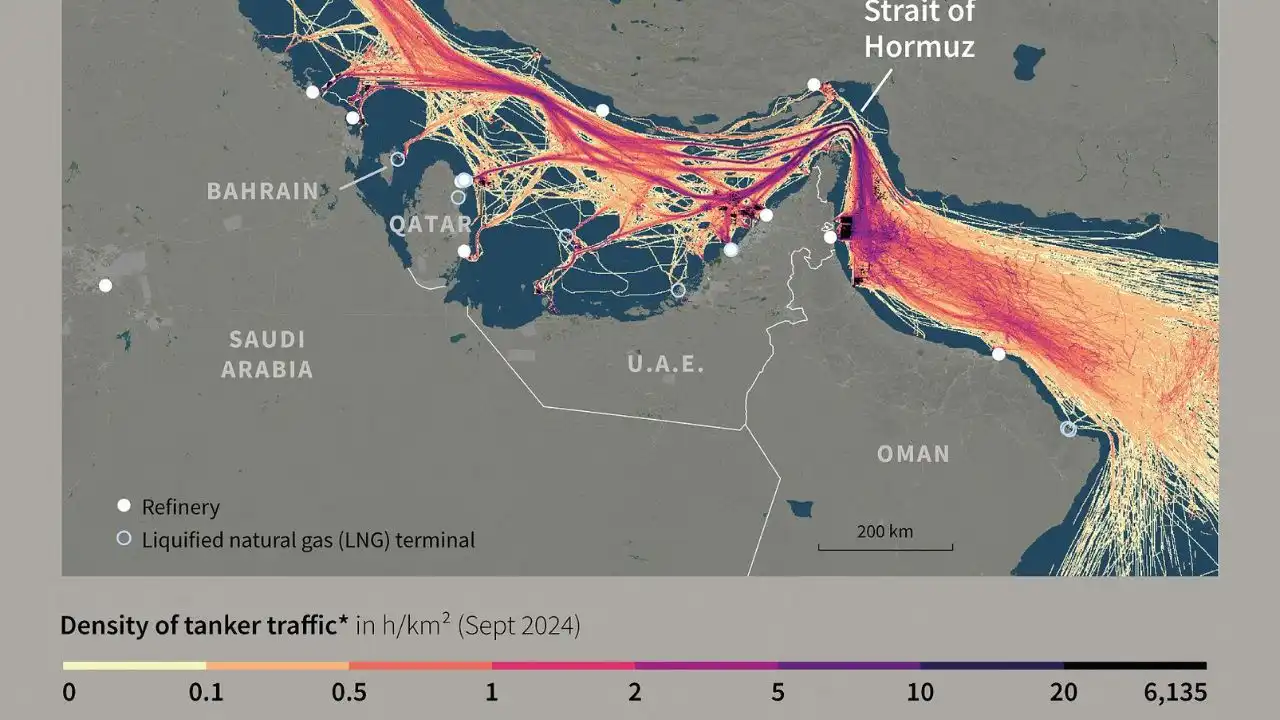

Middle East Tensions: Impact on India Trade & Oil

- March 02, 2026

Intel CEO Warns of Huawei’s Chip Talent Push

- February 28, 2026

Amazon to Invest $50B in OpenAI, Expands AWS Tie-Up

- February 28, 2026